The prevailing narrative on Wall Street suggests the American consumer is doing just fine. Economists point to low unemployment, steady retail sales, and a stock market that refuses to quit as evidence of a resilient public. They see a "soft landing" or perhaps no landing at all. But this data-driven optimism misses the structural rot beneath the surface. The American consumer is not thriving; they are surviving on a diet of expensive credit and depleted savings that cannot last.

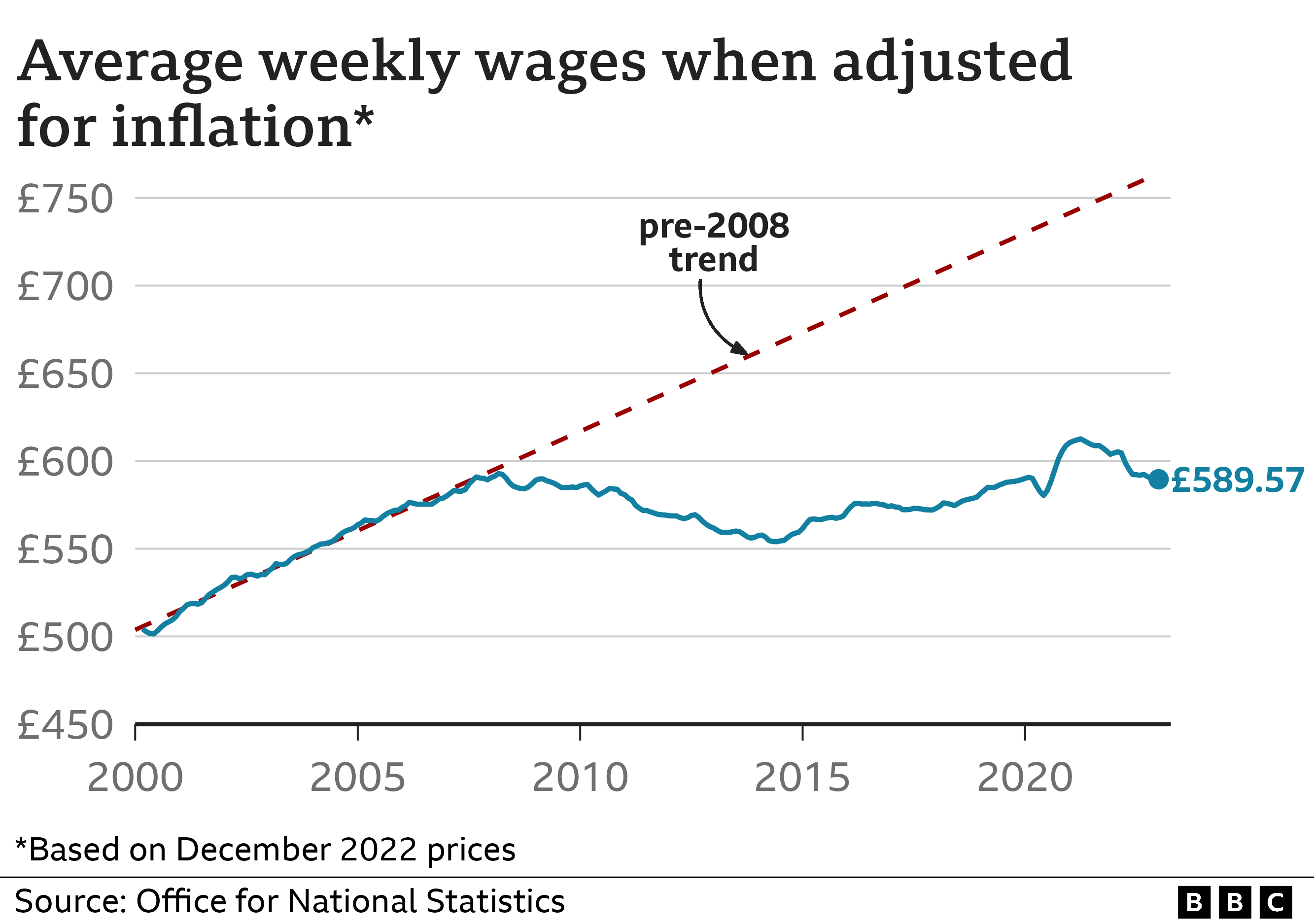

While headline figures show spending is up, they rarely account for the fact that people are paying more for less. Inflation has cooled in terms of its rate of increase, but the price level itself remains structurally higher than it was three years ago. The average household is now caught in a vice between stagnant real wages and the rising cost of basic necessities. To bridge the gap, they have turned to the only tool left in the box: debt.

The Credit Card Life Raft

Total household debt reached a record $17.69 trillion in early 2024. Credit card balances alone have surged, not because people are buying luxury goods, but because the math of daily life no longer adds up. For decades, the middle class relied on cheap money. When interest rates were near zero, carrying a balance was a manageable sin. Today, with average APRs hovering near 22 percent, that same balance has become a financial death sentence.

We are seeing a bifurcated economy. High-income earners with fixed-rate mortgages and significant stock portfolios are indeed doing well. Their wealth is tethered to assets that inflate alongside the currency. However, the bottom 60 percent of the population is experiencing a different reality. They are renters or recent buyers facing high monthly payments, and their primary "asset" is a paycheck that buys 20 percent less than it did in 2021.

Delinquency rates are the "canary in the coal mine" that the optimist crowd ignores. Credit card and auto loan transitions into serious delinquency are rising at a pace not seen since the 2008 financial crisis. This isn't just a statistical blip. It represents millions of households who have officially run out of runway. When a consumer stops paying their car note, they aren't making a lifestyle choice; they are signaling that the system has broken.

The Buy Now Pay Later Mirage

One reason retail sales look "okay" is the explosion of Buy Now, Pay Later (BNPL) services. This is "phantom debt" that often flies under the radar of traditional credit reporting agencies. It allows a consumer to split a $100 grocery bill into four easy payments. On paper, that grocery sale looks like healthy consumer demand. In reality, it is a desperate measure to keep the fridge full until the next direct deposit hits.

The Hidden Cost of Convenience

BNPL services market themselves as a friendly alternative to credit cards. They aren't. They are a high-velocity debt trap designed to encourage spending that the user cannot afford. Because these loans are often small and short-term, users stack them. It is not uncommon for a single household to have five or six active BNPL plans across different platforms. This creates a fragmented debt profile that makes it nearly impossible for the consumer to track their actual outflows.

The lack of transparency in this sector means the "resilient" consumer might be much closer to a cliff than the Federal Reserve realizes. If traditional credit is the front door to a debt crisis, BNPL is the basement window. It keeps the wheels of commerce turning in the short term, but it builds no long-term equity and offers no protection when the music finally stops.

The Housing Lock-In Effect

The American dream of homeownership has become a trap for those who already have it and a nightmare for those who don't. Millions of homeowners are sitting on 3 percent mortgage rates. They cannot afford to move because a similar house at today’s 7 percent rates would double their monthly payment. This has effectively killed the "starter home" market, as nobody is selling.

For the "OK" consumer to remain "OK," they need mobility. They need the ability to move for a better job or downsize to save money. That mobility is gone. We are witnessing the "Golden Handcuffs" of the 2020s. This lack of inventory keeps prices artificially high, which further punishes the young workers who are supposed to be the next engine of economic growth.

The Rental Squeeze

Those who aren't locked into low mortgages are getting hammered by the rental market. While some reports suggest rents are stabilizing, they are stabilizing at peaks that consume 40 to 50 percent of the average worker's take-home pay. This is the definition of a fragile consumer. When half your income goes to a landlord, there is zero margin for error. A medical emergency, a car repair, or a temporary layoff becomes a catastrophic event.

The Depletion of Pandemic Cushions

During the pandemic, American households built up a massive stockpile of "excess savings." Stimulus checks, paused student loan payments, and a lack of travel options created a temporary buffer. For the last two years, the economy has been running on the fumes of that cash pile.

Various estimates from the San Francisco Fed and private banks suggest that this buffer is now gone. The middle and lower-income brackets have exhausted their reserves. This explains why spending remained high even as inflation spiked—people were spending their savings to maintain their standard of living. Now that the bank accounts are empty, we are entering the period of "true" consumer strength, and the early signs are not encouraging.

The Psychology of the "Vibecession"

Economists are baffled by the "Vibecession"—the phenomenon where the data looks good, but people feel terrible about the economy. This isn't a mass delusion. It is a rational response to the loss of purchasing power and the disappearance of the financial safety net.

The American consumer feels precarious because they are precarious. They see the price of a Big Mac doubling. They see their insurance premiums jumping 20 percent in a single year. They see their utility bills climbing. The "top-down" data points like GDP growth don't pay the electric bill.

The Corporate Profit Margin Factor

We must also look at "greedflation" or margin expansion. Corporate profits as a share of GDP reached record highs recently. Many firms used the cover of global supply chain issues to raise prices far beyond their actual cost increases. This shifted wealth directly from the consumer’s wallet to the shareholder’s dividend check.

While this makes for a great stock market, it is a self-limiting strategy. You cannot strip-mine the consumer forever. Eventually, the buyer hits a wall where they simply cannot pay. We are seeing the first cracks in the fast-food industry, where giants like McDonald's and Taco Bell are suddenly scrambling to introduce "value meals" because they realized they had finally priced out their core demographic.

The Student Loan Reality Check

The resumption of student loan payments has pulled billions of dollars out of the monthly economy. For three years, that money was spent on retail, dining, and travel. Now, it is going back to the Treasury. This is a direct contractionary force on consumer spending that has yet to be fully realized in the quarterly data.

Consider a household that suddenly has to find an extra $400 a month. They don't just stop buying $400 worth of clothes. They cut back across the board. They switch to store brands. They cancel one of their four streaming services. They skip the weekend trip. This "death by a thousand cuts" is how a consumer-led recession begins.

The Employment Mirage

The low unemployment rate is the final shield for the "consumer is OK" argument. But look closer at the types of jobs being created. There is a notable shift toward part-time work and "side hustles." The "Gig Economy" is often a polite term for people who can't make ends meet with a single full-time job.

If a worker needs three jobs to pay the rent, they are technically "employed," but they are not a stable pillar of the economy. They are one missed shift away from insolvency. Furthermore, the massive white-collar layoffs in the tech and finance sectors suggest that even the "upper-middle" consumer is starting to feel the chill. These are the people who drive high-end discretionary spending, and they are currently updating their resumes.

The Inevitable Pivot

The American consumer is currently an acrobat performing a high-wire act without a net. They have used every trick in the book to keep their spending levels up—credit cards, BNPL, tapping home equity, and draining pandemic savings. But the wire is running out.

The next six to twelve months will reveal the truth. As the "lagged effects" of high interest rates finally permeate every corner of the household budget, the illusion of the bulletproof consumer will evaporate. Retailers will report "challenging environments." Banks will increase their loan-loss reserves. The media will act surprised.

The reality was always there in the math. You cannot have a healthy consumer base when the cost of living outpaces the reward for labor for a sustained period. The "OK" consumer was a mirage built on the remnants of a zero-interest-rate world that no longer exists.

Check the delinquency trends in your local zip code through public credit data. The numbers don't lie, even if the headlines do.